20,000 sounds like a lot. It sounds like a house down payment. It sounds like early retirement.

It is also a completely meaningless number.

In the startup world, 20,000 shares could be worth $2,000,000, or it could be worth enough to buy a slightly used Honda Civic. Without knowing the denominator, the numerator is useless. Here is the unvarnished math you need to do before signing that offer letter.

Step 1: Ask for the Outstanding Shares

If a recruiter refuses to tell you the total number of outstanding fully-diluted shares, run. Do not walk. Run.

You cannot calculate your ownership percentage without this number. If you have 20,000 shares and there are 20,000,000 shares outstanding, you own 0.1% of the company. If there are 200,000,000 shares outstanding, you own 0.01%.

The Script: "I am very excited about the offer. To help me evaluate the equity component, could you share the total number of fully-diluted outstanding shares, as well as the preferred price from the most recent funding round?"

Step 2: The Strike Price vs. Preferred Price

Your options will have a "strike price" (or exercise price). This is what it costs you to buy the shares. This is usually based on a 409A valuation, which is artificially low for tax purposes.

The "preferred price" is what the venture capitalists paid in the last round. The difference between these two numbers is the current theoretical value of your grant.

If your strike price is $1.00, and the VCs just paid $5.00, your 20,000 shares have a current theoretical value of $80,000 ((5 - 1) * 20,000). Not bad.

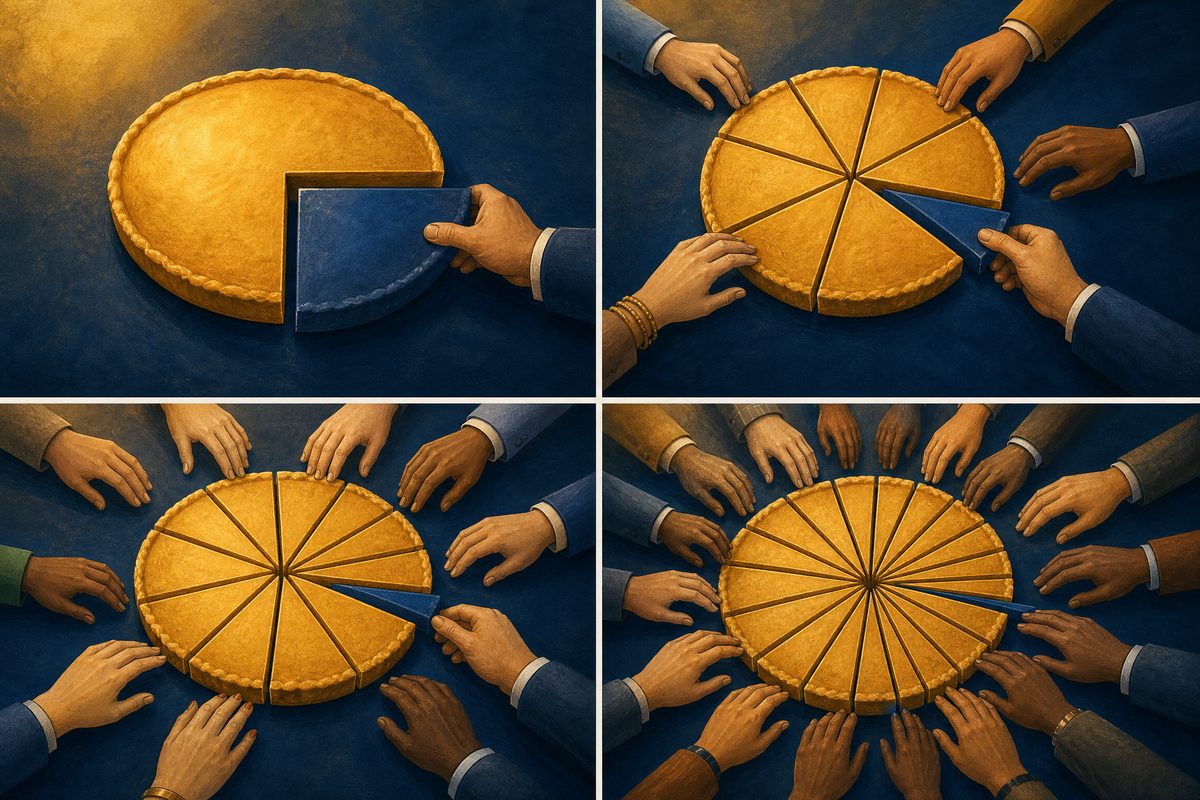

Step 3: The Dilution Discount

Here is the part recruiters conveniently forget to mention. If the company is currently at Series B, they will likely raise a Series C, a Series D, and maybe an E before an exit.

Every time they raise money, they issue new shares. Your 0.1% ownership will get diluted. A safe rule of thumb is to assume 15-20% dilution per future funding round.

If you expect three more rounds before an IPO, multiply your current percentage by 0.8 cubed (0.8 * 0.8 * 0.8 = 0.51). Your 0.1% at Series B will likely be ~0.05% at IPO.

Step 4: The Liquidation Preference Reality Check

This is the darkest math of all. Investors hold "preferred stock." You hold "common stock."

If the company sells for less than what the investors put in, the investors get their money back first. You get zero.

If a company raised $100M, and gets acquired for $90M, the founders get nothing. You get nothing. The VCs get $90M.

When you do your math, do not just model the $1 Billion unicorn exit. Model the $150M acqui-hire exit. If your math shows you making zero dollars in a mediocre outcome, you need to negotiate harder on your base salary.

Equity is a lottery ticket. It is a very fun lottery ticket, but you should never use it to pay your rent.